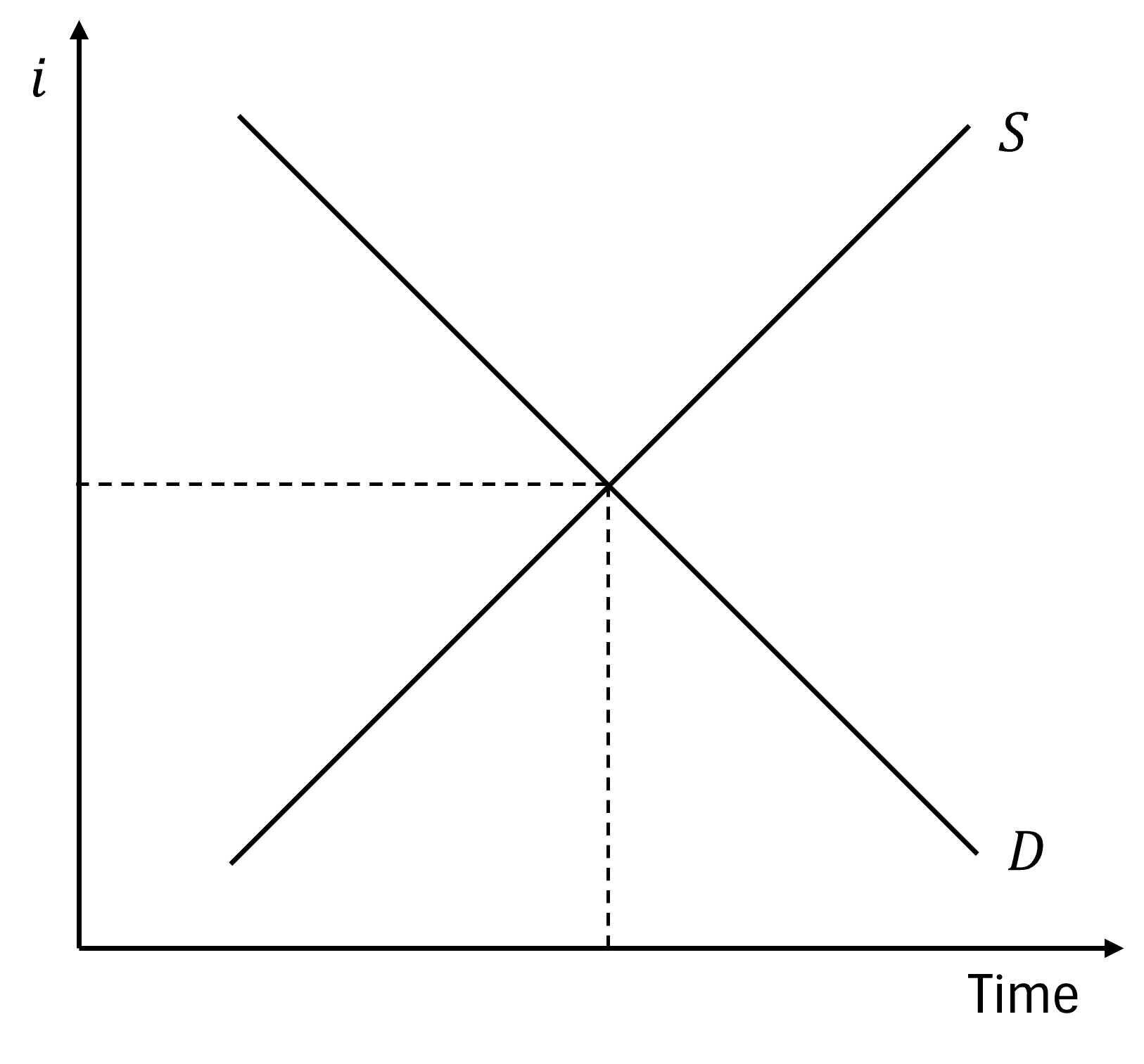

Interest rate as price of time: The interest rate is the price of time — the premium paid to access resources now rather than later — not the price of money. It exists in barter economies with no money present. The price of money is 1/P (purchasing power), as defined in Chapter 1. The “money market” in finance terminology refers to short-term credit instruments, not to money in the economic sense — a naming convention, not a conceptual equivalence.

Real vs. nominal rates and the Fisher equation: The nominal interest rate \(i\) is the rate written on a contract. The real interest rate \(r\) adjusts for expected inflation: \(r \approx i - \pi^e\). The Fisher equation \(i \approx r + \pi^e\) implies that lenders demand nominal rates high enough to cover both their real return and expected purchasing power erosion. Persistent high inflation therefore produces persistent high nominal rates. Central banks control nominal rates directly; real rates — which govern actual economic decisions — depend on the gap between nominal rates and inflation expectations.

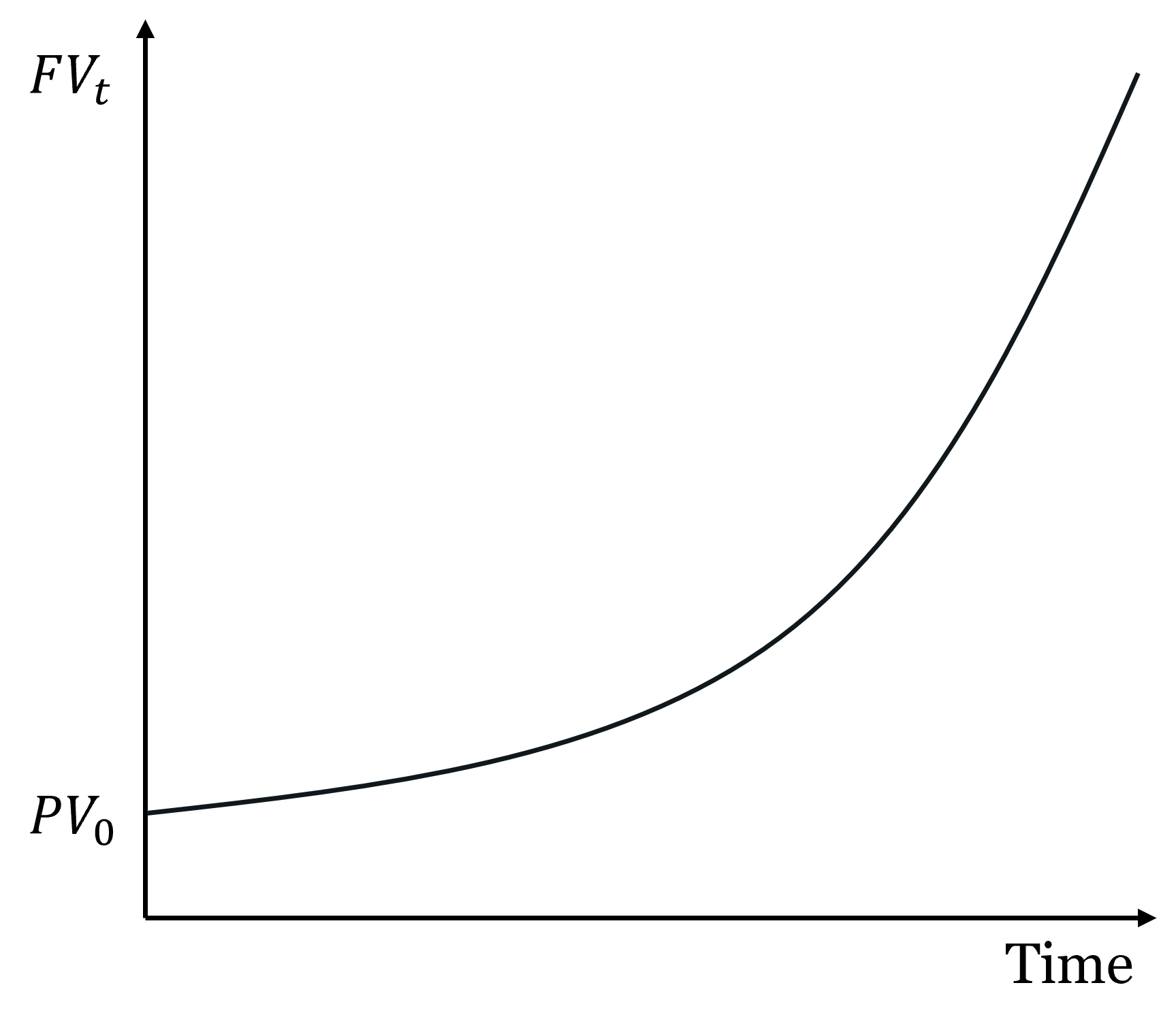

Future value and present value: Future value is the growth of a present sum through compounding: \(FV_n = PV \times (1+i)^n\). Present value is the current worth of a future cash flow: \(PV = CF_t / (1+i)^t\). For a stream of cash flows: \(PV = \sum CF_t / (1+i)^t\). The discount rate in the PV formula represents the opportunity cost of funds — the return available on the best alternative investment of similar risk. Present value is the universal valuation tool for financial assets.

Duration and interest rate sensitivity: Duration measures the weighted average time to receive cash flows and the sensitivity of an asset’s price to interest rate changes. Long-duration assets lose more value when rates rise than short-duration assets. A 1 percentage point rise in rates reduces a 5-year duration asset by approximately 5%, a 10-year duration asset by approximately 10%. This is the mechanism behind the inverse bond price-yield relationship and explains SVB’s vulnerability to the 2022–2023 rate cycle.

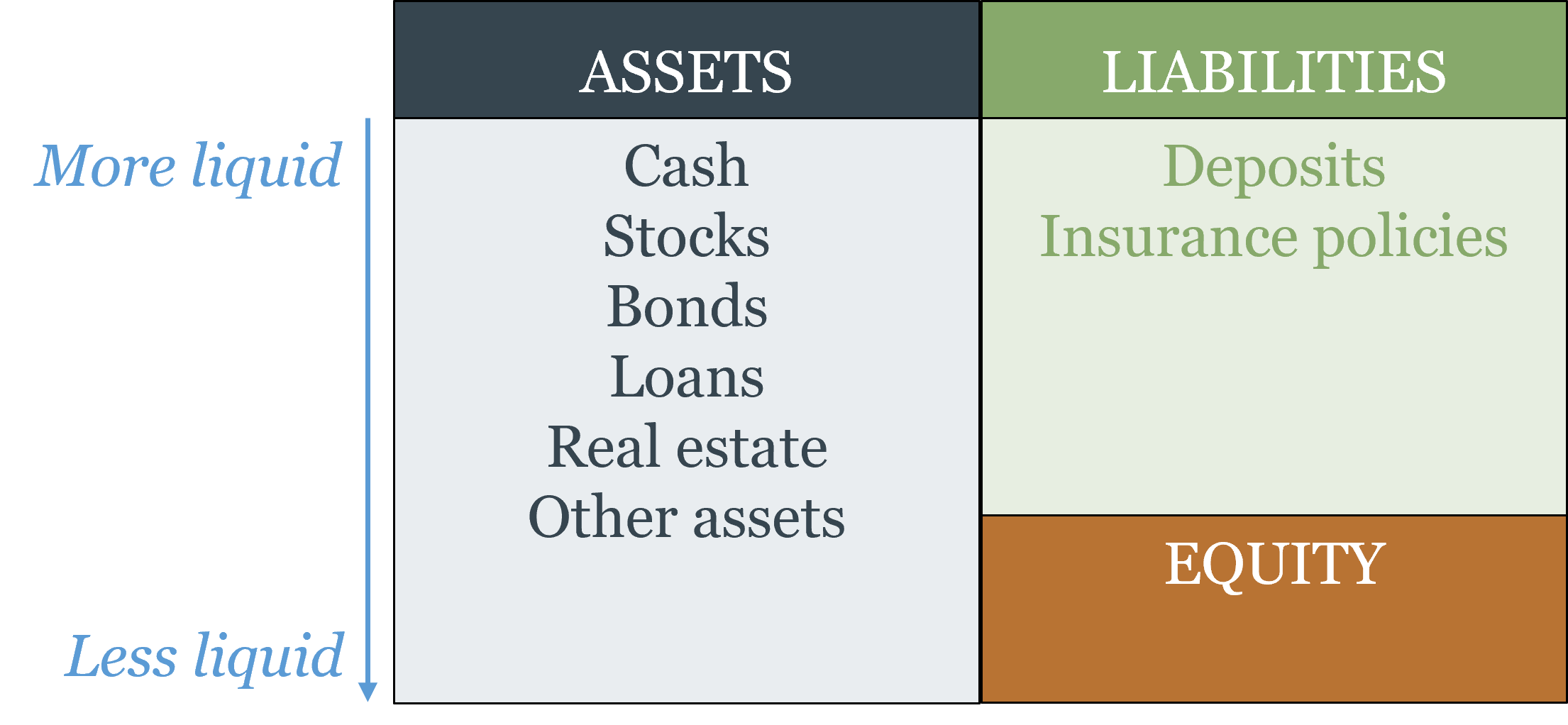

The financial system: Financial markets channel resources across time (from savers to borrowers), share and diversify risk, and aggregate dispersed information into prices. Direct finance connects borrowers to savers through markets; indirect finance uses intermediaries. Primary markets issue new securities (issuers receive proceeds); secondary markets trade existing securities (issuers receive nothing, but liquidity in secondary markets enables primary issuance). Financial instruments include debt (fixed senior claims), equity (residual ownership claims), and derivatives (contracts whose value derives from underlying assets).

Asymmetric information: When one party to a transaction has relevant information the other lacks, two problems arise. Adverse selection (pre-transaction): the parties most eager to transact tend to be those for whom it is most advantageous to themselves. Akerlof’s lemons model shows this can destroy markets from the top down. In financial markets, adverse selection makes equity issuance expensive and drives good firms away. Moral hazard (post-transaction): once a contract is in place, one party’s behavior changes in ways that harm the other. In equity financing, managers with diluted ownership have weakened incentives to maximize firm value (the principal-agent problem). In debt financing, borrowers have incentives to take excessive risk (heads I win, tails you lose). Solutions include disclosure requirements, intermediary screening, collateral requirements, and signaling mechanisms. None fully solves these problems — which is why financial regulation exists, and why financial crises recur.